Japan’s Puzzle - The Interplay of Shifting Forces

Macro Insights

QuantCube’s latest insights into Japan’s economic outlook

A Paradigm in Motion

Japan's economy is undergoing a historic paradigm shift, moving beyond three decades of deflation and weak-yen dependency. The end of Yield Curve Control (YCC) has become a critical catalyst for transition, reinforced by substantial wage gains from the 2024 Shunto negotiations, which have bolstered the Bank of Japan (BoJ)’s confidence in sustained reflation. Alternative data highlight the key forces driving this change: moderate inflation, resurgent domestic demand, and a robust tourism recovery. Together, they are reshaping the investment landscape of the world’s fourth-largest economy.

Markets Pricing Goldilocks

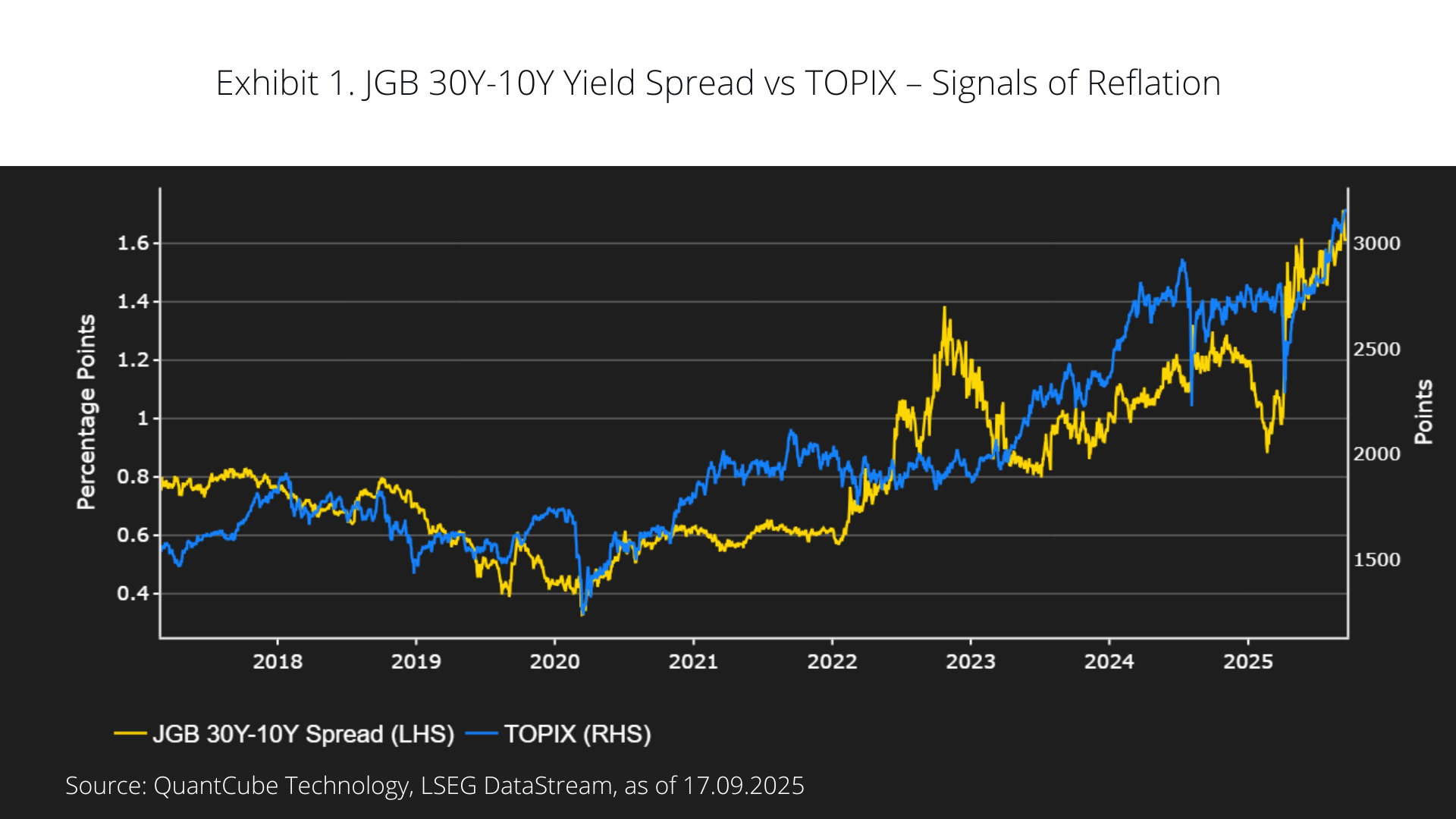

Exhibit 1 illustrates how markets are positioning for both rate normalization and sustainable growth. The widening of the JGB 30Y–10Y spread indicates investor anticipation of the BoJ’s gradual exit from ultra-loose monetary policy, while the parallel upward trend of the yield curve and the TOPIX since 2023 reflects a structural shift toward “reflation” and “interest rate normalization”. Shorter-term divergences, however, reveal tactical swings in sentiment, driven by the push-and-pull between BoJ interventions, external shocks, and market positioning.

Beyond the Debt Narrative

Japan’s transition is not without risks: its immense public debt makes fiscal sustainability sensitive to real rates. Yet this is balanced by deep buffers —corporate cash reserves, household savings, net foreign assets, and the yen’s role as a natural hedge—all of which provide resilience and policy flexibility.

Another underappreciated force is the structural shift in defense spending. Geopolitical pressures, amplified by US defense policy under Trump and beyond, have pushed Japan to take greater responsibility for its own security. Domestic defense-related industries are expanding their role in developing advanced technologies, adding a new dimension of growth to Japan’s industrial base.

The puzzle is therefore less about whether change is happening, and more about whether Japan can manage these shifting forces without undermining fiscal stability.

Inflation – The Central Issue

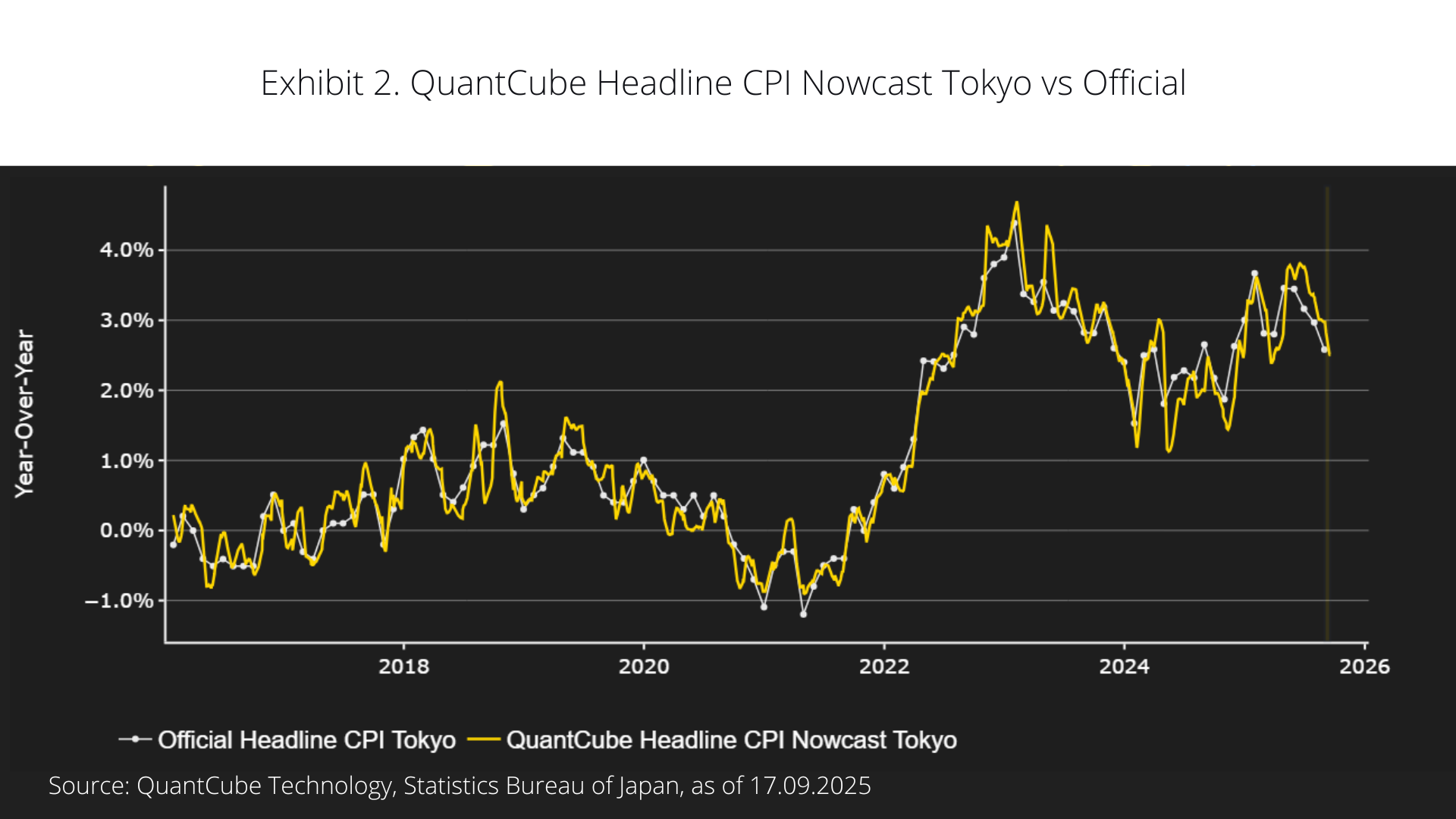

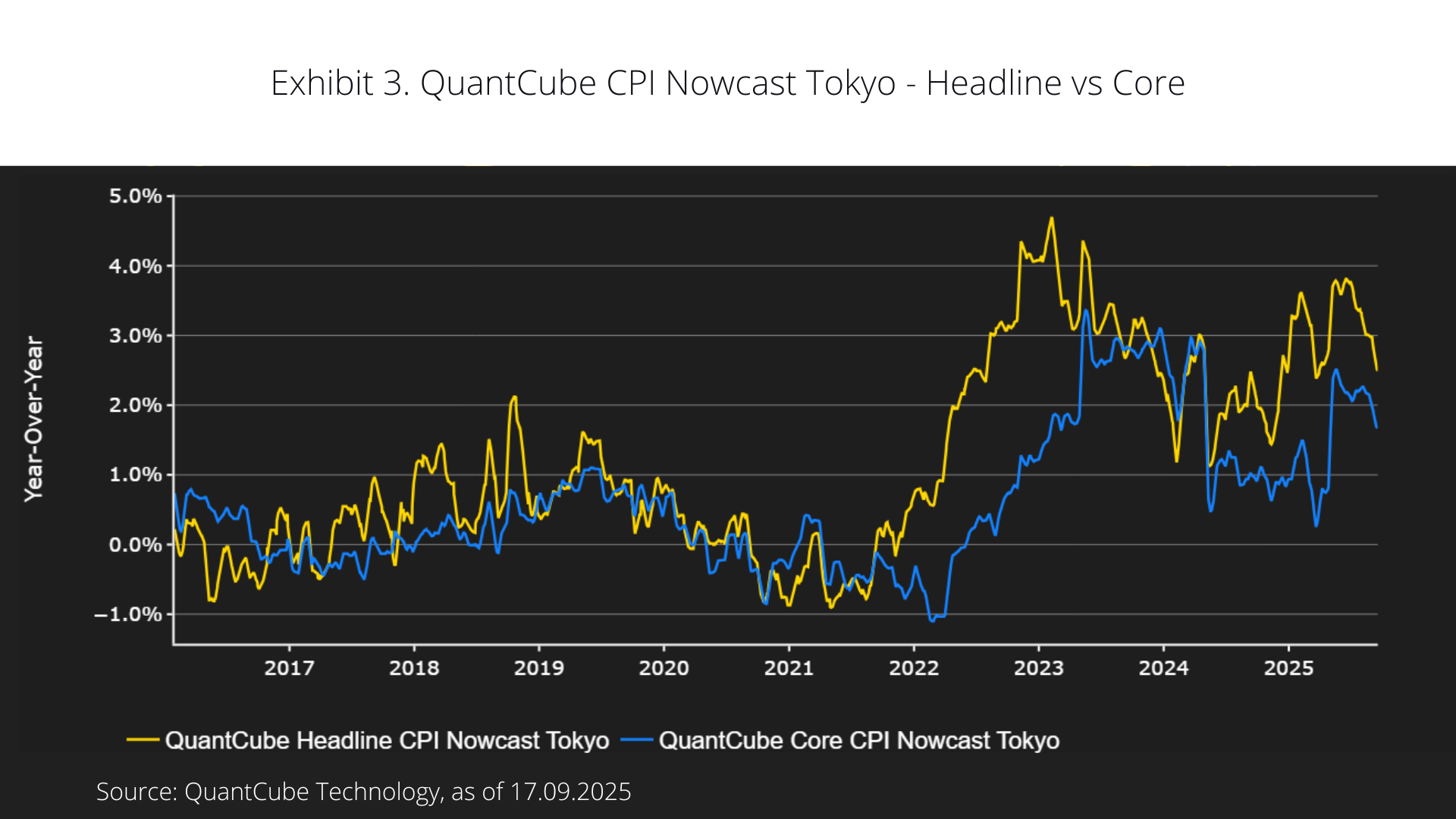

Inflation remains at the heart of Japan’s economic transition. A sustained pickup in prices has driven interest rates higher and continues to challenge the BoJ’s ability to normalize policy. For much of the past two years, producer price inflation (PPI) has hovered around 2%, pointing to relatively soft imported inflation. This has given Japan a window to shift from an externally driven, import-cost model toward a more sustainable framework anchored in domestic demand. Encouragingly, core inflation is now converging more closely with headline measures, suggesting that price dynamics are becoming more internally generated. (Exhibit 2 and 3)

Inflation’s New Anchors – Demographics, Politics, and the Yen

The durability of this trend is tied increasingly to structural anchors. Demographics - an aging population and a shrinking labor force, partly offset by immigration – are beginning to exert upward pressure on wages and services prices. Politics also matter: inflation has sharpened populist sentiment, as seen in recent elections, weakening government stability and complicating reform momentum. At the same time, external pressures – notably the impact of new U.S. tariffs – add uncertainty to the inflation outlook.

Additionally, the yen plays a dual role: while weakness amplifies imported inflation, its status as a safe-haven currency also cushions shocks during global downturns. This makes Japan’s inflation path especially sensitive to shifts in external conditions.

With the BoJ’s first rate hike in early 2025 making a historic step away from ultra-loose policy, the central bank now has incentives to pause, weighing durability of domestic inflation against risks from trade tensions and political ambiguity.

Signs of Growth

Energy Demand

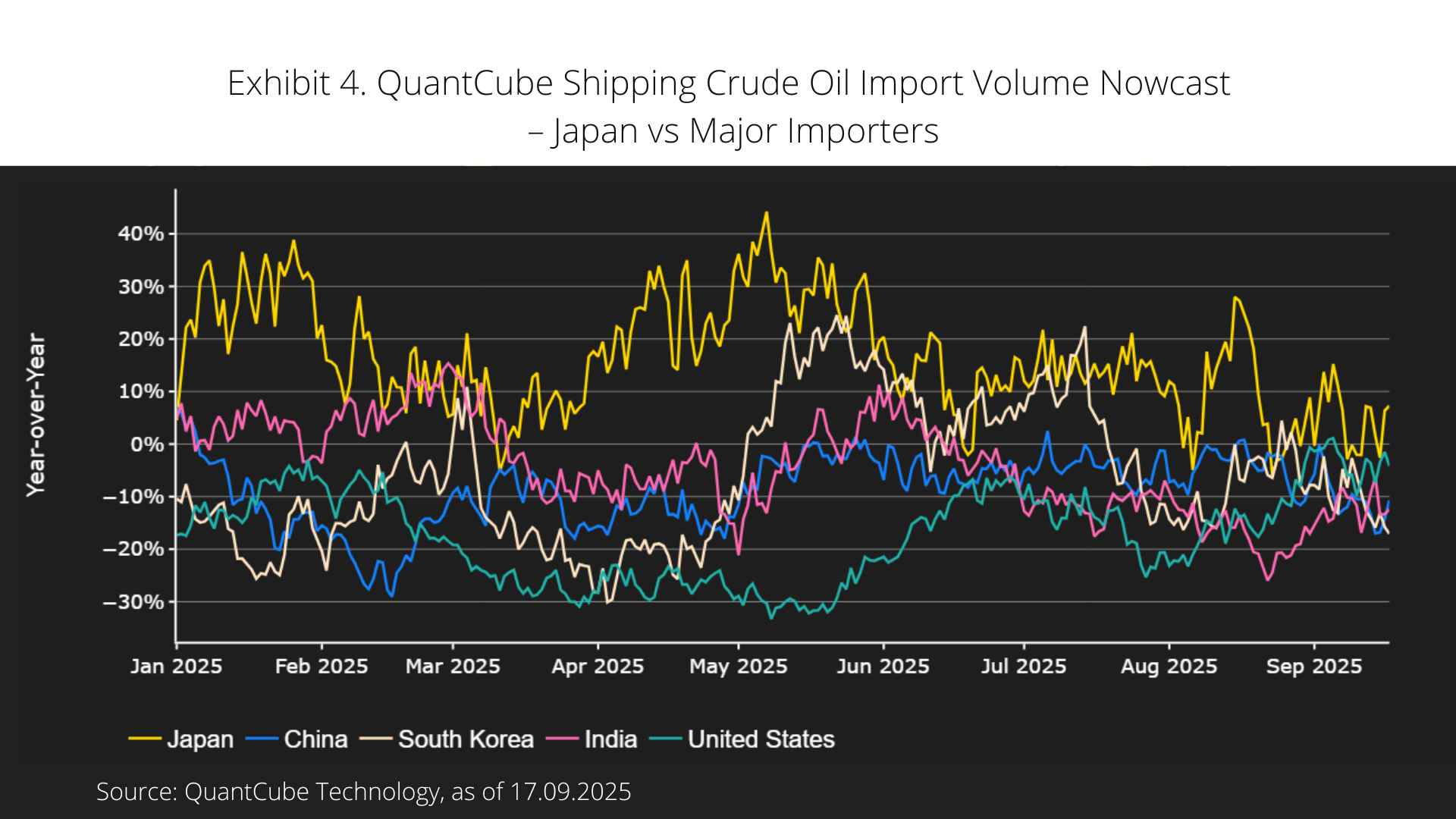

QuantCube Shipping Crude Oil Import Volume Nowcast (Exhibit 4) reveals a striking divergence in oil import dynamics among the world’s top five importers over the past year. The United States (–4.2%), South Korea (–17.2%), India (–12.4%), and China (-10.7%) all registered year-on-year declines, consistent with weaker global growth, tighter monetary conditions, and the structural shift toward renewables. Japan, however, stands out as the clear outlier as Exhibit 4 illustrates. Oil imports surged by +7.3%, the only positive figure among its peers and by far the strongest. This resilience suggests that Japan’s energy demand is not merely stable but expanding at a time when others are scaling back.

Possible drivers include: a revival in energy-intensive manufacturing, precautionary stockpiling to hedge against supply disruptions, and strategic recalibration of energy policy to enhance and reduce external vulnerabilities.

In contrast to the global downtrend, Japan’s import trajectory underscores both its distinct industrial dynamics and its policy of energy security – a key pillar of its broader growth story.

Heart of Manufacturing – Nagoya's Industrial Pulse

Nagoya, Japan’s largest manufacturing hub and home to global leaders such as Toyota, Mitsubishi Heavy Industries, and Brother Industries, offers a powerful lens into the country’s industrial backbone. With its deep specialization in the automobile and aerospace sectors, the city’s performance is a bellwether for Japan’s broader industrial cycle.

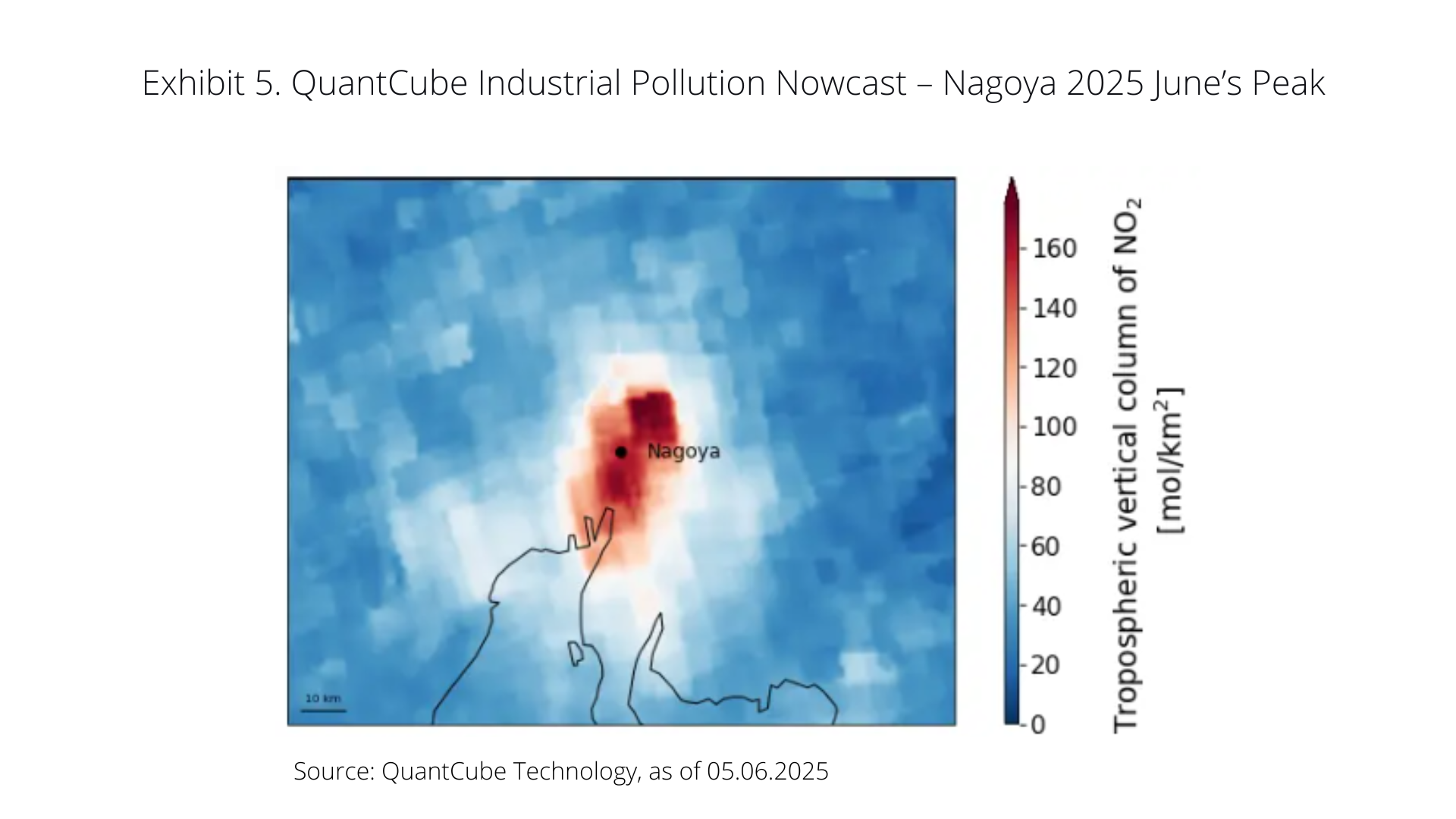

Exhibit 5 highlights how QuantCube’s Industrial Pollution Indicator captured a sharp surge in atmospheric NO2 concentrations on June 5, 2025—the highest level recorded that month. This spike signals an intense, high-frequency burst of industrial activity and energy consumption, offering real-time evidence of resurgent momentum within Nagoya’s manufacturing base.

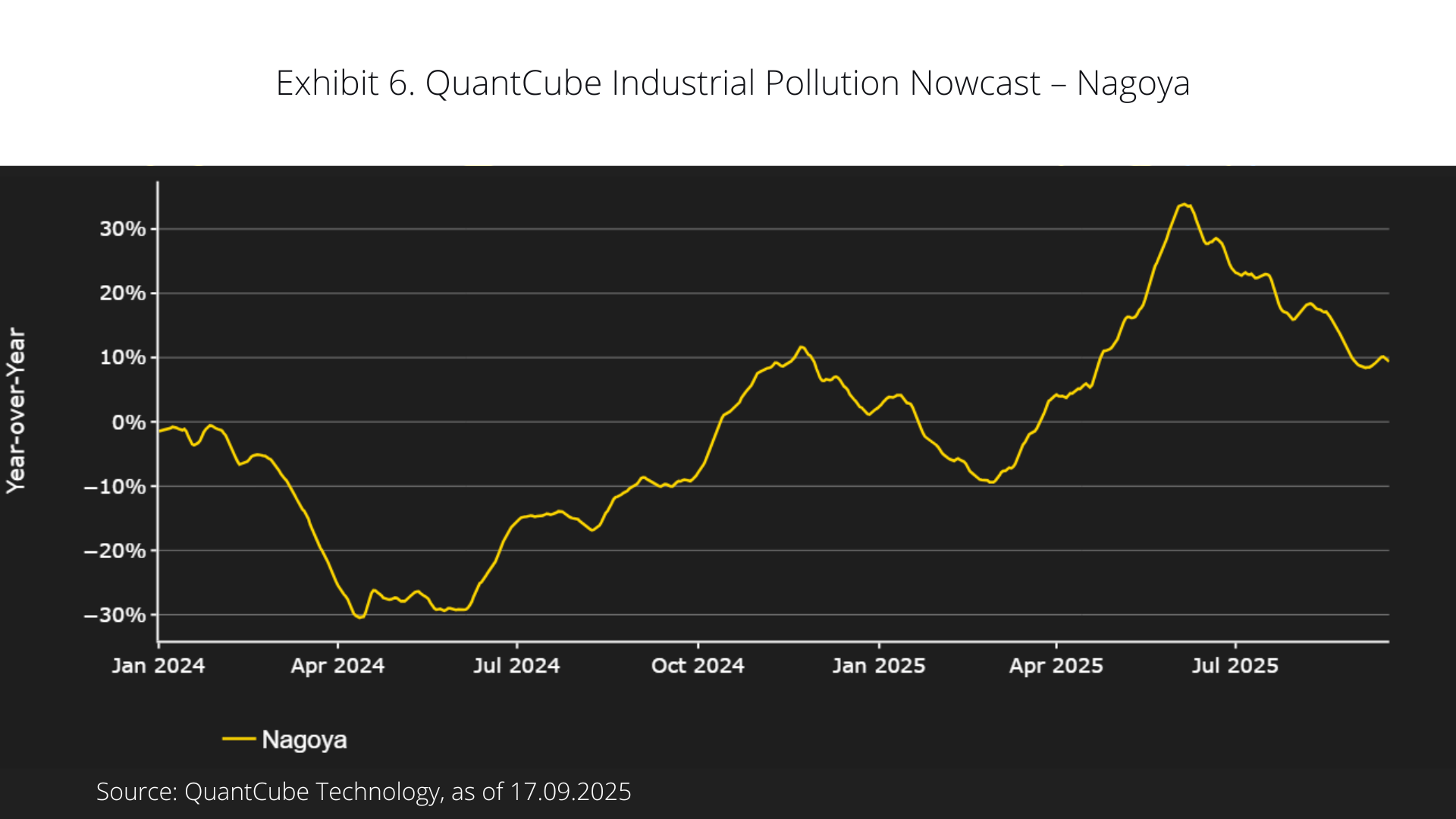

While QuantCube’s Industrial Pollution Nowcast – Nagoya (Exhibit 6) reveals a strong recovery from mid-2024 lows to a peak of over +30% year-on-year by mid-2025, the broader 18-month trend still reflects robust industrial momentum and resilience. This recovery underscores not only Japan’s industrial backbone but also Nagoya’s critical role in anchoring the shift toward more domestically driven growth.

That said, this momentum now faces a near-term headwind. The deceleration observed since July 2025 is highly likely the lagged repercussion of US tariff policies, the full impact of which materialized after the Liberation Day. This suggests that the exogenous shock of trade friction is now tempering the strong endogenous growth narrative, presenting a key test for the region’s industrial resilience.

Tourism – A Strategic Amplifier, not Just a Pillar

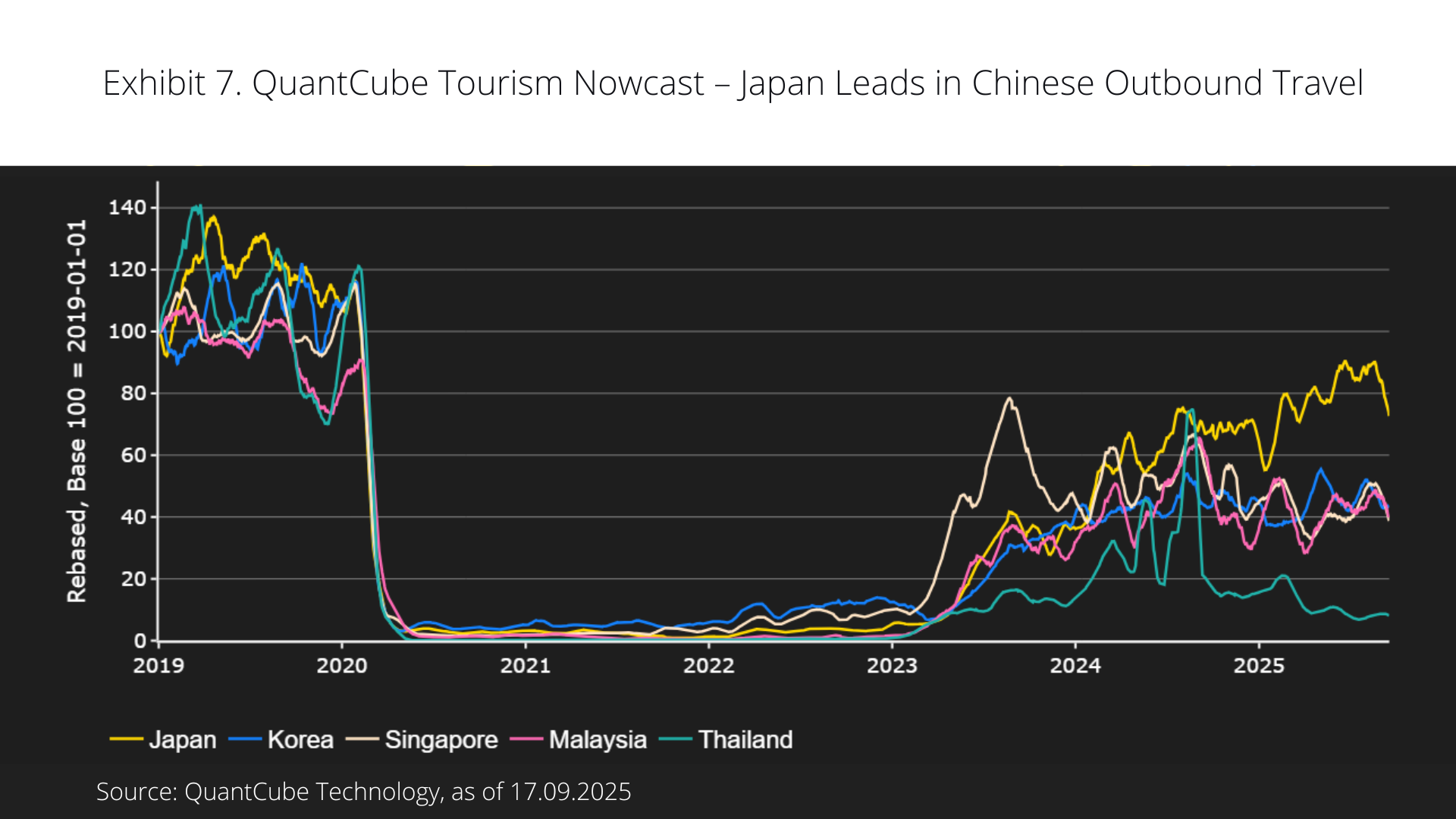

Japan’s tourism sector is experiencing a strong rebound, supported by the recovery in global flight capacity and the steady return of inbound flows from Korea, Southeast Asia, and most importantly China. As Exhibit 7 illustrates, Chinese tourists, in particular, have reemerged as the dominant driver of volume and spending, leveraging the weak yen to maximize purchasing power across retail, dining, and luxury goods.

While tourism directly contributes only around 1.5% - 2% of total GDP, its macroeconomic significance is far greater than this headline number suggests. Tourism acts as a strategic amplifier of demand, bolstering consumer-facing industries and reinforcing Japan’s policy push to cultivate “inbound demand” as a growth engine. Its impact is especially visible at the sectoral and regional level: for accommodation, food & beverage, retail (notably duty-free), and regional transport, tourism inflows provide the difference between stagnation and sustained recovery.

In this sense, tourism is less about being the single “pillar” of Japan’s services economy and more about serving as a shock absorber and accelerator, cushioning downturns in domestic consumption while stimulating local economies disproportionately reliant on external visitors.

Puzzle Reassembling

Japan is navigating a complex but promising transition from its post-bubble era model. The paradigm shifts toward moderate inflation and interest rate normalization—underpinned by resurgent industrial activity, corporate reinvestment, and booming tourism sector—lays the groundwork for more sustainable, domestically driven growth. Importantly, this evolution is not simply cyclical but structural: companies are deploying their deep balance-sheet reserves, wage dynamics are strengthening, and strategic investment in areas such as defense and green technology is reshaping the industrial base.

Yet the challenges remain profound. The nation's colossal public debt burden means that the trajectory of real interest rates is critical—nominal growth must consistently outpace borrowing costs to safeguard fiscal sustainability. The BoJ faces a delicate balancing act, its credibility contingent on delivering durable inflation above 2% while avoiding a sharp rise in debt-servicing costs. Domestic political pressures and external trade frictions further complicate this path.

Ultimately, Japan’s puzzle is being reassembled into a more balanced and resilient economic framework—less dependent on a weak yen and more grounded in domestic demand, corporate strength, and strategic sectors. The final picture will depend on policymakers’ ability to manage the interplay of these shifting forces, ensuring that the long-awaited normalization enhances rather than undermines fiscal and macro stability.