Key macroeconomic developments in 2023 – and outlook for 2024

Macro Insight

2023 macro recap and 2024 outlook for US and China

As US headline inflation eases in December: is there more room for the Fed to cut rates in the new year?

In our observation, US inflation in 2023 was shaped by two key factors. Firstly, the Federal Reserve raised interest rate repeatedly to curb price rises. Their ultimate goal was to bring inflation down to its target levels. However, this effort was hampered by the second factor: significant global constraints in commodity supplies. At QuantCube, we have been monitoring daily changes in the US Headline Consumer Price Index (CPI) using alternative data. Real-time trend analysis for CPI components can provide important insights into the potential future actions of the Fed with regard to interest rates. In April 2023, the QuantCube US Core Services Inflation Indicator successfully captured a downward trend in Core Services CPI, a key metric for assessing longer-term inflationary pressure. This was a significant development as the Federal Reserve considers the signal as one of the key factors for its rate policy decisions. We observed the downward trend in Core Services CPI a month ahead of the release of official data, and it was later confirmed by government statistics. This led to the Fed's decision to pause its rate hikes in June.

Our analysis in July this year pointed to a marked increase in the food and energy components of the CPI after the decision by Russia and Saudi Arabia to curtail oil exports. Recently the inflation outlook started to improve with notably downward trends in Headline CPI. This is giving the Fed board an opportunity to consider potential rate cuts in the near future. However, the Fed needs to tread carefully in our view. As Exhibit 1 shows, QuantCube US CPI Nowcast levels are still significantly above the US inflation target; +4.1% for core inflation with the services component recording +5.1% as of December 21.

Furthermore, the recent crisis in the Red Sea might complicate the Fed’s efforts to combat inflation. Attacks from Houthi rebels in Yemen on shipping vessels have escalated since mid-December in response to the war in Gaza, targeting The Bab el-Mandeb Strait, one of the world’s major chokepoints at the southern end of the Red Sea. According to the Institute of Export and International Trade, approximately 12% of global trade passes through the Red Sea. Any disruptions in this vital trade route could have far-reaching implications for international trade flows and commodity prices. Due to increasing threats in the region, prominent shipping companies including BP and Maersk have decided to re-route their cargos around Africa to avoid the affected area. If this situation persists, it may drive oil prices higher, therefore jeopadising the prospects of interest rate cuts in 2024. Using real-time data we will continue to evaluate the potential impact on the global economy. At the moment it is too early to say if the situation is serious enough to pose a threat to the global supply of goods and commodities.

US Job Openings reach lowest level in one year

The Federal Reserve's policy decisions are also heavily influenced by labor market conditions. In particular, the Fed pays significant attention to the official monthly jobs reports. With QuantCube’s Job Openings Nowcast Indicator we can gain early insights into the US job market. As of December 18, the indicator stood at its lowest point in a year as Exhibit 2 shows. The recent sharp decline in job openings suggests that elevated interest rates are beginning to impact the demand for labor. Will the weak labor market conditions continue ? In our view, additional signs that confirm a cooling labor market are required before future interest rate cuts.

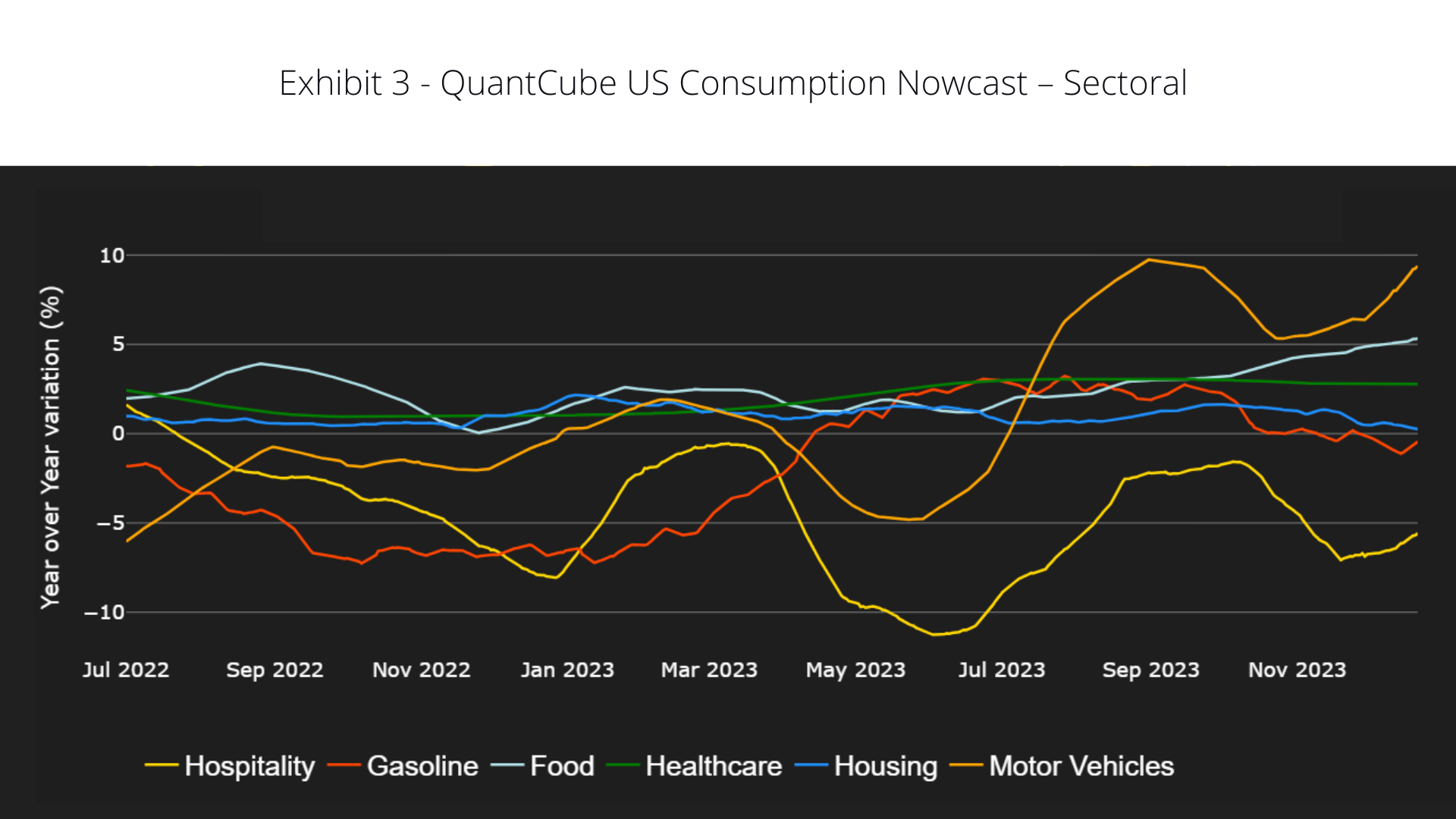

US consumer spending is trending upwards as the inflation outlook improves

Based on real-time alternative data, we track private consumption at country and sectoral levels on a daily basis. The analysis provides insights into real-time consumption trends, up to three months in advance of the publication of official numbers.

Exhibit 3 shows sectoral consumption levels in the US using the QuantCube Consumption Nowcast Indicator. It seems that domestic demand for discretionary goods (motor vehicles, gasoline), and hospitality services have been trending upwards since the end of November. This is most likely due to improving consumer confidence as a result of easing inflation. The US consumer seems resilient as the holiday season starts, but we will wait and see if the upward trend in US consumption continues into 2024. Uncertainty still remains regarding households’ behaviour once they face the reality of dwindled savings and tighter credit conditions after the holiday period.

Chinese Industrial activity: a sign of increasing outputs before the New Year Holidays

Our NO2 concentration indicator, a real-time proxy for industrial activity in China, is now increasing in line with seasonal trends as Exhibit 4 demonstrates. In China, industry usually makes a concerted effort to meet production deadlines before the New Year Holiday period. However, in some regions including Wuhan, the area renowned for automotive production, NO2 concentration has not yet reached the level of previous years, suggesting a full-blown economic recovery remains some way off.

In contrast, the industrial outlook appears slightly more optimistic in the Southeast region, particularly around Guangzhou, a key hub for export-oriented industries such as semi-conductors. Here, NO2 levels are more consistent with or above those of previous years. This regional disparity underscores the uneven nature of China's industrial recovery and points to a complex landscape for future economic growth in China. Exhibit 5 shows the QuantCube Consumption Nowcast for China. The indicator remains weak overall with consumption rates in Culture/Education/Recreation and Residence particulary affected.

While the recovery of China’s domestic consumption still remains wobbly, there is a sign that China’s export activites are increasing. Exhibit 6 shows the QuantCube International Trade Nowcast for Chinese container exports. It seems that Chinese container exports are generally increasing, with India recording a particularly strong increase in recent months. The level of exports of goods to the US too is reporting a higher level compared to one year ago.

While there are some signs of recovery in certain sectors and regions, the overall picture of China's economic resurgence is still mixed in our view. This has implications not only for domestic policy and economic planning in China but also for global supply chains and international trade, given China's integral role in these areas.